The war in Iran: rising energy prices and their impact

Launching operation ‘Epic Fury’, the US and Israel attacked several targets in Iran on Saturday 28 February. Ayatollah Khamenei and other high-ranking government officials and military leaders were killed during the strikes, prompting Iran to fire missiles at Israel, US allies and US bases. The oil infrastructure in Iran and other Middle Eastern countries is increasingly under attack and Iran threatened to close the Strait of Hormuz, a crucial choke point for oil and gas transport. Although it has not yet followed through on this threat, shipping traffic through the Strait of Hormuz has virtually ground to a halt.

While Donald Trump has stated that the war will end “soon”, there is still great uncertainty about how the conflict will evolve. The longer the conflict lasts and the more it escalates, the larger its impact on global economic developments. The main consequences include higher energy prices, higher shipping prices, higher resin prices (affecting food prices globally) and aluminium prices, disrupted supply chains, and adverse effects on business and consumer confidence as a result of the increased uncertainty.

Impact on the energy markets

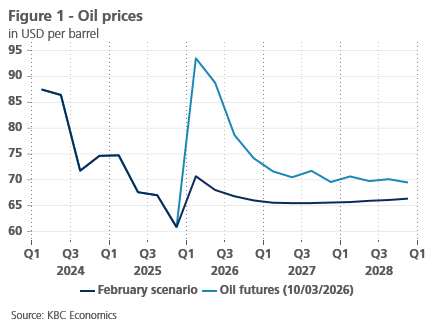

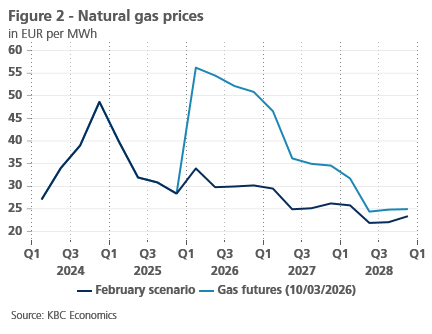

The rising energy prices will have the largest economic impact, and the energy markets remain highly volatile. Oil prices are currently 32% higher than when we prepared our scenario in February (see Figure 1), and TTF natural gas prices are even up more than 67% (see Figure 2). The futures markets show smaller increases, which suggests that the markets expect the situation to stabilise in the medium term.

However, further escalation could exert significant upward pressure on energy prices. The Middle East accounts for roughly 30% of global oil production and 17% of global natural gas production. Some 20% of global oil stocks and global LNG flows pass through the Strait of Hormuz. Iran itself supplies 4.5% of global oil production and 7% of global natural gas production.

Economic impact

The recent increase in oil and gas prices is likely to have a slightly negative impact on the growth of both the US and the European economy, given the temporary nature of the shock (according to the futures). It is also worth noting that the European and US economies have greatly reduced their dependence on oil and gas in the past few decades, which has improved their resilience to energy shocks. Having said that, the economic shock would become more severe if energy prices were to rise further and remain elevated for an extended period of time.

The current increase in energy prices is likely to have a larger impact on inflation, especially in the euro area, where natural gas prices have gone up considerably. The US still has prices under control with its largely domestic natural gas market. Inflation expectations for the next 12 months have indeed risen faster in the euro area than in the US (see Figure 3). Long-term inflation expectations remain well anchored for the time being.

Consequences for central banks

The stagflationary nature of the present energy price shock presents a dilemma for banks. The immediate inflationary effect of the current shock will keep US inflation above the target level and will drive up euro area inflation to above the target level, but the downside risks to growth and employment will make many central banks reluctant to severely tighten their monetary policies in response to the shock. Nevertheless, the markets are currently expecting just one interest rate cut by the Fed this year (as opposed to two cuts before the war).

This shift occurred despite a favourable inflation report and a poor labour market report (revealing a loss of 92,000 jobs in February). The markets expect the ECB to announce two interest rate hikes this year, which, as mentioned above, is likely due to the greater inflationary impact in the euro area. It should be stressed that there is great uncertainty in this regard. If oil and gas prices were to rise even further and the shock were to become permanent, central banks would be able to pursue more restrictive policies.

Disclaimer:

Unless expressly stated otherwise, all the information you consult or obtain here has a non-binding and purely informative value. It is updated to the best of our ability and at regular intervals. However, KBC Bank NV does not guarantee that this information is up-to-date, accurate, correct, complete or suitable for a particular purpose. The information provided here does not constitute advice or an offer to sell products or services and is not intended for commercial use. You remain fully responsible for the consequences of the use you make of this information. The intellectual property rights to the information, publications and data provided here belong to KBC Bank NV or third parties and you must refrain from any infringement thereof. Except with the express prior and written consent of KBC Bank NV, any transfer, sale, distribution or reproduction of this information is prohibited.