Economic recovery in Germany: waiting for Godot?

For many years, Germany was considered the indestructible engine of Europe, but that engine has been sputtering for quite some time now. The continent’s largest economy is barely growing and its industrial model is under pressure, raising the question of whether Berlin is finally ready to change course. What’s happening in Germany today is more than a temporary slump – it’s about finding the path to a new economic era.

The most telling figure is also the most perplexing: Germany’s real GDP today is still roughly at the same level as it was at the beginning of 2018. While other major economies have recovered after the pandemic, Germany continues to mark time. The United States’ performance has improved, Spain is clearly catching up, France is holding up better than expected and even Italy is now doing better than in the years before Covid-19. This is a sobering observation for a country that for decades symbolised industrial strength, strong exports and economic stability.

Those hoping that this is just a classic cyclical dip are underestimating the gravity of the situation. After all, the slowdown of German growth started before the pandemic. Covid-19, the energy crisis and geopolitical tensions have magnified the problems but did not cause them. What we see today is mainly the erosion of an economic model that relied on the same formula for too long: strong exports, industrial dominance, cheap energy and a near-ideological aversion to budget deficits.

That old model is now losing momentum on several fronts at the same time. Investment in machinery and equipment is lagging, construction activity is weakening, goods exports are lower than before, and household consumption is barely making a meaningful contribution to growth. What remains is mostly government consumption, supplemented by a limited boost from investments in ICT. But that is not a solid foundation for a sustainable economic recovery. Rather, it is a sign that the traditional private growth engines have started to sputter.

Opvallend is dat Duitsland niet in de eerste plaats lijdt aan een klassiek loonkostenprobleem. Natuurlijk spelen kosten een rol, zeker na de recente energiecrises, maar de kern van de malaise ligt dieper. De Duitse economie botst op structurele grenzen in een wereld die fundamenteel verandert. Geopolitieke fragmentatie, toenemende handelsconflicten, de energietransitie, digitalisering en de nood aan technologische vernieuwing zetten het land onder druk om zichzelf opnieuw uit te vinden. Duitsland moet niet alleen herstellen, het moet zich heruitvinden.

Interestingly, the classic problem of labour costs is not Germany’s principal issue. Of course costs play a role – especially after the recent energy crises – but the root of the problem lies deeper. The German economy is running into structural limits in a world that is changing fundamentally. Geopolitical fragmentation, increasing trade conflicts, the energy transition, digitalisation and the need for technological innovation are putting pressure on the country to reinvent itself. Germany needs to do more than recover – it needs to find a new identity.

On top of that, the international environment has become much more hostile for Germany. The renewed competitive pressure from China is hitting precisely those sectors in which Germany traditionally excelled, such as the automotive industry and mechanical engineering. As a result, the trade surplus Germany could build on for years is less and less of a given. Meanwhile, energy remains a vulnerability, especially for an economy with a large and energy-intensive industrial base. New price shocks or geopolitical escalations could therefore quickly undermine recovery again.

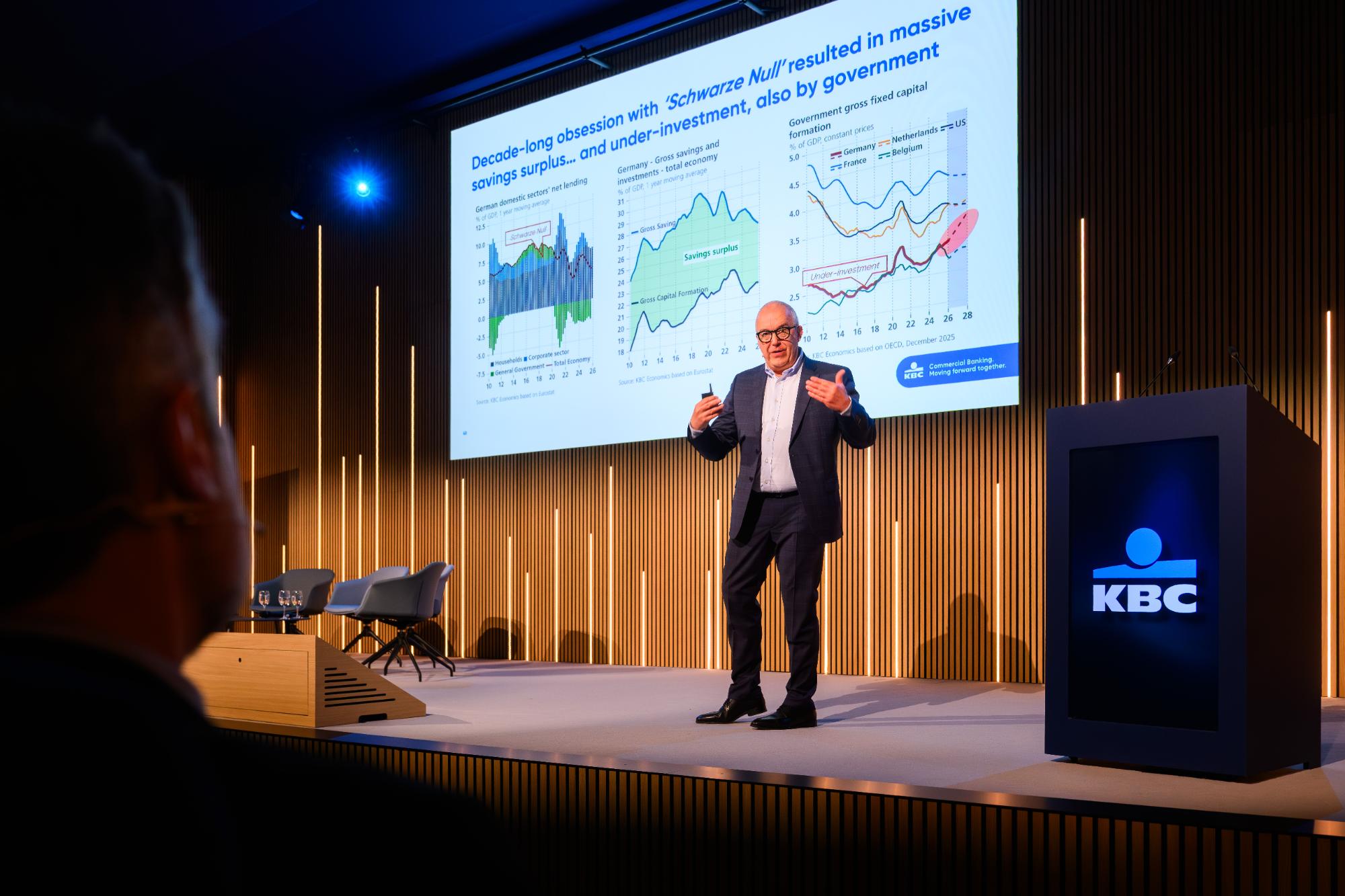

But part of the responsibility also lies with Berlin itself. For many years, Germany stuck to its ‘Schwarze Null’ policy, framing a balanced budget as the ideal. That budgetary rigour produced a large savings surplus, but also led to substantial underinvestment in infrastructure, digitalisation and public modernisation. This macro-economic paradox is now backfiring: an economy that saves heavily but invests too little in its own future saddles itself with ageing and weaker growth.

This is precisely why fiscal policy now stands to have the greatest impact. The hope is that Germany can embark on an atypical recovery driven not by conventional export growth, but by targeted public investment in defence, climate policy, infrastructure, energy and digitalisation. Under Chancellor Merz, that policy shift has been cautiously announced, but there is still a gap between intention and implementation for the time being. The expected deficits have not yet materialised to the same extent as hoped, and it is precisely this hesitant implementation that is fuelling economic uncertainty.

That uncertainty is reflected in the behaviour of households and businesses. The tendency to save remains exceptionally high and the labour market is starting to show signs of weakening, despite being surprisingly resilient for a long time. This situation is risky, as weakening confidence could delay recovery for months or even years. At the same time, this also presents an opportunity, because once confidence returns, those hoarded savings could translate into additional consumption and investment. If so, Germany could recover faster than is currently expected.

For now, the outlook remains mixed. The growth forecast for 2026 has recently been revised downwards, but recovery is still expected to be possible. This would bring a temporary uptick in inflation, albeit one much less sharp than during the previous energy crisis, meaning the ECB wouldn’t need to raise interest rates again. However, much depends on factors that Germany itself doesn’t fully control, such as changes to the price of energy, international trade and geopolitical conflicts.

Germany is therefore not just facing a straightforward recovery, but a much more profound challenge. The country needs to move away from an economic model that worked extremely well for years but is now visibly straining under the weight of new global conditions. The real question is not whether growth will ever return, but whether Germany will succeed in building a new model where investment, innovation and strategic resilience take centre stage. Europe’s economic engine is still running, but its sound is becoming less and less familiar.

Stay updated

You’ll soon find the second part of our series on Germany on our website. Be sure to also check out our news overview with articles on other economic topics.

Disclaimer:

Tenzij uitdrukkelijk anders bepaald, heeft alle informatie die u hier raadpleegt of verkrijgt een vrijblijvende en zuiver informatieve waarde. Ze wordt naar best vermogen en op regelmatige tijdstippen bijgewerkt. KBC Bank NV geeft echter geen garanties wat betreft de actualiteit, accuraatheid, correctheid, volledigheid of geschiktheid voor een bepaald doel van deze informatie. De hier verstrekte informatie vormt geen advies of verkoopaanbod van producten of diensten en is niet bestemd voor commercieel gebruik. U blijft zelf volledig aansprakelijk voor de gevolgen van het gebruik dat u van deze informatie maakt. De intellectuele eigendomsrechten op de informatie, publicaties en gegevens die hier verstrekt worden, komen toe aan KBC Bank NV of aan derden en u moet zich onthouden van elke inbreuk hierop. Behoudens de uitdrukkelijk voorafgaande en schriftelijke toestemming van KBC Bank NV is elke overdracht, verkoop, verspreiding of reproductie van deze informatie verboden.